Compare Strategies

| SYNTHETIC LONG CALL | LONG PUT LADDER | |

|---|---|---|

|

|

|

| About Strategy |

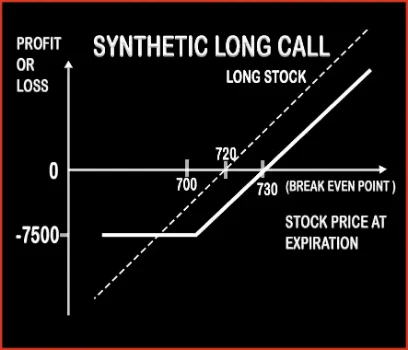

Synthetic Long Call Option StrategyA trader is bullish in nature for short term, but also fearful about the downside risk associated with it. Here, a trader wants to hold an underlying asset either in physical form like in case of commodities or demat (electronic) form in case of stocks. But he is always exposed to downside risk and in order to mitigate his losses, |

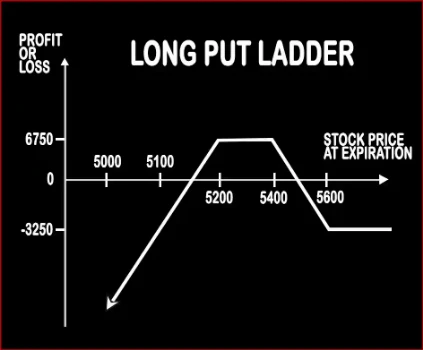

Long Put Ladder Option StrategyLong Put Ladder can be implemented when a trader is slightly bearish on the market and volatility. It involves buying of an ITM Put Option and sale of 1 ATM & 1 OTM Put Options. However, the risk associated with this strategy is unlimited and reward is limited. Risk:< .. |

SYNTHETIC LONG CALL Vs LONG PUT LADDER - Details

| SYNTHETIC LONG CALL | LONG PUT LADDER | |

|---|---|---|

| Market View | Bullish | Neutral |

| Type (CE/PE) | CE (Call Option) | PE (Put Option) |

| Number Of Positions | 2 | 3 |

| Strategy Level | Beginners | Advance |

| Reward Profile | When Price of Underlying > Purchase Price of Underlying + Premium Paid | Limited |

| Risk Profile | Limited (Maximum loss happens when the price of instrument move above from the strike price of put) | Unlimited |

| Breakeven Point | Underlying Price + Put Premium | Upper Breakeven Point = Strike Price of Long Put - Net Premium Paid, Lower Breakeven Point = Total Strike Prices of Short Puts - Strike Price of Long Put + Net Premium Paid |

SYNTHETIC LONG CALL Vs LONG PUT LADDER - When & How to use ?

| SYNTHETIC LONG CALL | LONG PUT LADDER | |

|---|---|---|

| Market View | Bullish | Neutral |

| When to use? | A trader is bullish in nature for short term, but also fearful about the downside risk associated with it. | This Strategy can be implemented when a trader is slightly bearish on the market and volatility. |

| Action | Buy 1 ATM Put or OTM Put | Buy 1 ITM Put, Sell 1 ATM Put, Sell 1 OTM Put |

| Breakeven Point | Underlying Price + Put Premium | Upper Breakeven Point = Strike Price of Long Put - Net Premium Paid, Lower Breakeven Point = Total Strike Prices of Short Puts - Strike Price of Long Put + Net Premium Paid |

SYNTHETIC LONG CALL Vs LONG PUT LADDER - Risk & Reward

| SYNTHETIC LONG CALL | LONG PUT LADDER | |

|---|---|---|

| Maximum Profit Scenario | Current Price - Purchase Price - Premium Paid | Strike Price of Long Put - Strike Price of Higher Strike Short Put - Net Premium Paid - Commissions Paid |

| Maximum Loss Scenario | Premium Paid | When Price of Underlying < Total Strike Prices of Short Puts - Strike Price of Long Put + Net Premium Paid |

| Risk | Limited | Unlimited |

| Reward | Unlimited | Limited |

SYNTHETIC LONG CALL Vs LONG PUT LADDER - Strategy Pros & Cons

| SYNTHETIC LONG CALL | LONG PUT LADDER | |

|---|---|---|

| Similar Strategies | Protective Put, Long Call | Short Strangle (Sell Strangle), Short Straddle (Sell Straddle) |

| Disadvantage | •Chances of loss if the underlying goes down. •Incur losses if option is exercised. | • Unlimited risk. • Margin required. |

| Advantages | •Limited risk, unlimited profit. •Protection to your long-term holdings. • Limited loss to the to the premium paid for Put option. | • Reduces capital outlay of bear put spread. • Wider maximum profit zone. • When there is decrease in implied volatility, this strategy can give profit. |