This strategy is implemented by a trader when he is neutral on the movements and bearish on volatility i.e. he expects the stock to be range bound in the near future. This strategy involves sale of 1 ITM Call Option and 1 ITM Put Option. This strategy can be called as Credit Spread since his account is credited at the time of entering in the positions.

This strategy is implemented by selling (short) the underlying asset in the cash/futures market. Simultaneously, sell ATM Puts double the number of long quantity. This strategy is used by a trader who in neutral on the market and bearish on the volatility in the near future. Here profits will be capped up to the premium amount and risk will be potentially unlimited. ..

Max Profit Achieved When Price of Underlying = Strike Price of Short Puts

Risk Profile

Unlimited

Loss Occurs When Price of Underlying < Strike Price of Short Put - Net Premium Received OR Price of Underlying > Strike Price of Short Put + Net Premium Received

Breakeven Point

Upper Breakeven Point = Net Premium Received + Strike Price of Short Call, Lower Breakeven Point = Strike Price of Short Put - Net Premium Received

Upper Breakeven Point = Strike Price of Short Puts + Points of Maximum Profit Lower Breakeven Point = Strike Price of Short Puts - Points of Maximum Profit

SHORT GUTS Vs RATIO PUT WRITE - When & How to use ?

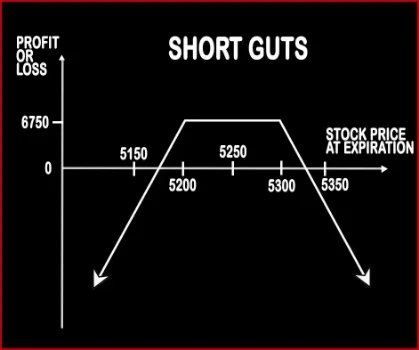

SHORT GUTS

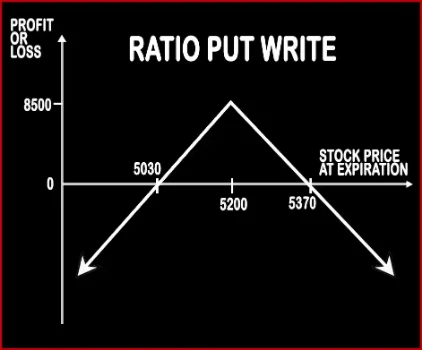

RATIO PUT WRITE

Market View

Neutral

Neutral

When to use?

This strategy is implemented by a trader when he is neutral on the movements and bearish on volatility i.e. he expects the stock to be range bound in the near future.

This strategy is implemented by selling (short) the underlying asset in the cash/futures market. This strategy is used by a trader who in neutral on the market and bearish on the volatility in the near future

Action

Sell 1 ITM Call, Sell 1 ITM Put

Sell 2 ATM Puts

Breakeven Point

Upper Breakeven Point = Net Premium Received + Strike Price of Short Call, Lower Breakeven Point = Strike Price of Short Put - Net Premium Received

Upper Breakeven Point = Strike Price of Short Puts + Points of Maximum Profit Lower Breakeven Point = Strike Price of Short Puts - Points of Maximum Profit

SHORT GUTS Vs RATIO PUT WRITE - Risk & Reward

SHORT GUTS

RATIO PUT WRITE

Maximum Profit Scenario

Net Premium Received + Strike Price of Short Put - Strike Price of Short Call - Commissions Paid

Net Premium Received - Commissions Paid

Maximum Loss Scenario

Price of Underlying - Strike Price of Short Call - Net Premium Received OR Strike Price of Short Put - Price of Underlying - Net Premium Received + Commissions Paid

Price of Underlying - Sale Price of Underlying - Net Premium Received OR Strike Price of Short Put - Price of Underlying - Net Premium Received + Commissions Paid

Risk

Unlimited

Unlimited

Reward

Limited

Limited

SHORT GUTS Vs RATIO PUT WRITE - Strategy Pros & Cons

SHORT GUTS

RATIO PUT WRITE

Similar Strategies

Short Strangle (Sell Strangle), Short Straddle (Sell Straddle)

Short Strangle and Short Straddle

Disadvantage

• Unlimited potential loss if the underlying stock continues to move in one direction. • High margin required.

• Potential loss is higher than gain. • Limited profit.

Advantages

• Ability to profit even when underlying asset stays stagnant. • You are already paid your full profit the moment the position is put on as this is a credit spread position. • Higher chance of ending in full profit as compared to short strangle or short straddle.