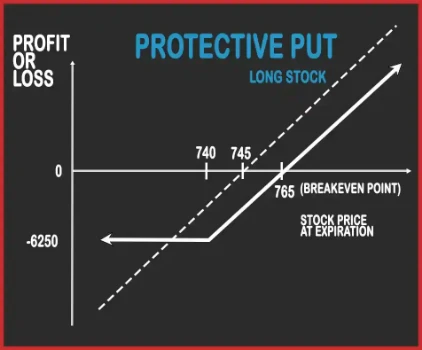

Protective Put Strategy is a hedging strategy where trader guards himself from the downside risk. This strategy is adopted when a trader is long on the underlying asset but skeptical of the downside. He will buy one ATM Put Option to hedge his position. Now, if the underlying asset moves either up or down, the trader is in a safe position.

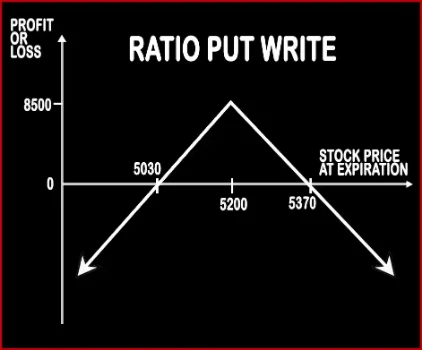

This strategy is implemented by selling (short) the underlying asset in the cash/futures market. Simultaneously, sell ATM Puts double the number of long quantity. This strategy is used by a trader who in neutral on the market and bearish on the volatility in the near future. Here profits will be capped up to the premium amount and risk will be potentially unlimited. ..

Max Profit Achieved When Price of Underlying = Strike Price of Short Puts

Risk Profile

Limited

Loss Occurs When Price of Underlying < Strike Price of Short Put - Net Premium Received OR Price of Underlying > Strike Price of Short Put + Net Premium Received

Breakeven Point

Purchase Price of Underlying + Premium Paid

Upper Breakeven Point = Strike Price of Short Puts + Points of Maximum Profit Lower Breakeven Point = Strike Price of Short Puts - Points of Maximum Profit

PROTECTIVE PUT Vs RATIO PUT WRITE - When & How to use ?

PROTECTIVE PUT

RATIO PUT WRITE

Market View

Bullish

Neutral

When to use?

This strategy is adopted when a trader is long on the underlying asset but skeptical of the downside.

This strategy is implemented by selling (short) the underlying asset in the cash/futures market. This strategy is used by a trader who in neutral on the market and bearish on the volatility in the near future

Action

Buy 1 ATM Put

Sell 2 ATM Puts

Breakeven Point

Purchase Price of Underlying + Premium Paid

Upper Breakeven Point = Strike Price of Short Puts + Points of Maximum Profit Lower Breakeven Point = Strike Price of Short Puts - Points of Maximum Profit

PROTECTIVE PUT Vs RATIO PUT WRITE - Risk & Reward

PROTECTIVE PUT

RATIO PUT WRITE

Maximum Profit Scenario

Price of Underlying - Purchase Price of Underlying - Premium Paid

Net Premium Received - Commissions Paid

Maximum Loss Scenario

Premium Paid + Purchase Price of Underlying - Put Strike + Commissions Paid

Price of Underlying - Sale Price of Underlying - Net Premium Received OR Strike Price of Short Put - Price of Underlying - Net Premium Received + Commissions Paid

Risk

Limited

Unlimited

Reward

Unlimited

Limited

PROTECTIVE PUT Vs RATIO PUT WRITE - Strategy Pros & Cons

PROTECTIVE PUT

RATIO PUT WRITE

Similar Strategies

Long Call, Call Backspread

Short Strangle and Short Straddle

Disadvantage

• Value of protective put position decreases as time passes • Holding period of the protective put can be affected by the timing as a result tax rate on the profit or loss from the stock can be affected.

• Potential loss is higher than gain. • Limited profit.

Advantages

• Unlimited potential profit due to indefinitely rise in the underlying stock price . • This strategy allows you to hold on to your stocks while insuring against losses. • Hedging strategy, trader can guard himself from the downside risk.