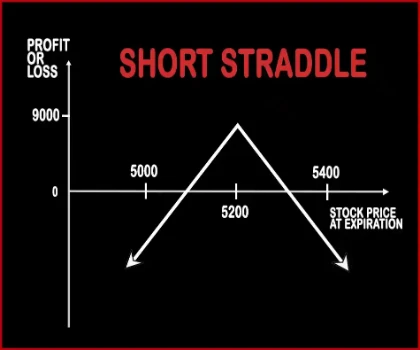

This strategy is just the opposite of Long Straddle. A trader should adopt this strategy when he expects less volatility in the near future. Here, a trader will sell one Call Option & one Put Option of the same strike price, same expiry date and of the same underlying asset. If the stock/index hovers around the same levels then both the options will expire worthless an

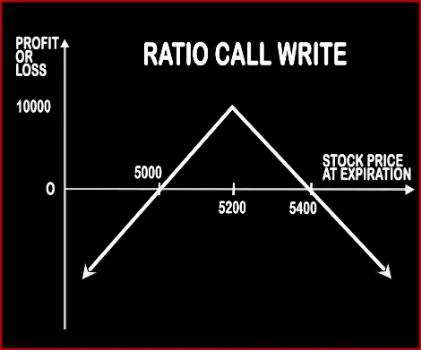

This strategy involves buying of an underlying asset in the cash/futures market and simultaneously selling ATM Calls double the number of long quantity. This strategy is used by a trader who is neutral on the market and bearish on the volatility in the near future. Here profits will be capped up to the premium amount and risk will be potentially unlimited.

Lower Breakeven = Strike Price of Put - Net Premium, Upper breakeven = Strike Price of Call+ Net Premium

Upper Breakeven Point = Strike Price of Short Calls + Points of Maximum Profit, Lower Breakeven Point = Strike Price of Short Calls - Points of Maximum Profit

SHORT STRADDLE Vs RATIO CALL WRITE - When & How to use ?

SHORT STRADDLE

RATIO CALL WRITE

Market View

Neutral

Neutral

When to use?

This strategy is work well when an investor expect a flat market in the coming days with very less movement in the prices of underlying asset.

This strategy is used by a trader who is neutral on the market and bearish on the volatility in the near future.

Action

Sell Call Option, Sell Put Option

Sell 2 ATM Calls

Breakeven Point

Lower Breakeven = Strike Price of Put - Net Premium, Upper breakeven = Strike Price of Call+ Net Premium

Upper Breakeven Point = Strike Price of Short Calls + Points of Maximum Profit, Lower Breakeven Point = Strike Price of Short Calls - Points of Maximum Profit

SHORT STRADDLE Vs RATIO CALL WRITE - Risk & Reward

SHORT STRADDLE

RATIO CALL WRITE

Maximum Profit Scenario

Max Profit = Net Premium Received - Commissions Paid

Net Premium Received - Commissions Paid

Maximum Loss Scenario

Maximum Loss = Long Call Strike Price - Short Call Strike Price - Net Premium Received

Price of Underlying - Strike Price of Short Call - Net Premium Received OR Purchase Price of Underlying - Price of Underlying - Net Premium Received + Commissions Paid

Risk

Unlimited

Unlimited

Reward

Limited

Limited

SHORT STRADDLE Vs RATIO CALL WRITE - Strategy Pros & Cons

SHORT STRADDLE

RATIO CALL WRITE

Similar Strategies

Short Strangle

Variable Ratio Write

Disadvantage

• Unlimited risk. • If the price of the underlying asset moves in either direction then huge losses can occur.

• Potential loss is higher than gain. • Limited profit.

Advantages

• A trader can earn profit even when there is no volatility in the market . • Allows you to benefit from double time decay. • Trader can collect premium from puts and calls option .