A trader shorts or writes a Call Option when he feels that underlying stock price is likely to go down. Selling Call Option is a strategy preferred for experienced traders.

However this strategy is very risky in nature. If the stock rallies on the upside, your risk becomes potentially unquantifiable and unlimited. If the strategy

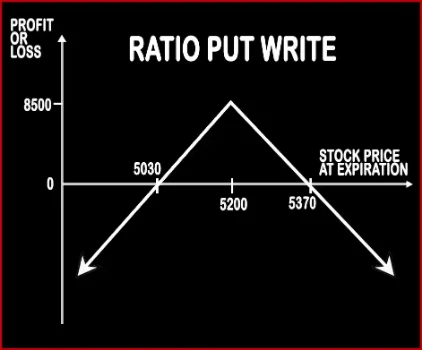

This strategy is implemented by selling (short) the underlying asset in the cash/futures market. Simultaneously, sell ATM Puts double the number of long quantity. This strategy is used by a trader who in neutral on the market and bearish on the volatility in the near future. Here profits will be capped up to the premium amount and risk will be potentially unlimited. ..

Max Profit Achieved When Price of Underlying = Strike Price of Short Puts

Risk Profile

Unlimited

Loss Occurs When Price of Underlying < Strike Price of Short Put - Net Premium Received OR Price of Underlying > Strike Price of Short Put + Net Premium Received

Breakeven Point

Strike Price of Short Call + Premium Received

Upper Breakeven Point = Strike Price of Short Puts + Points of Maximum Profit Lower Breakeven Point = Strike Price of Short Puts - Points of Maximum Profit

SHORT CALL Vs RATIO PUT WRITE - When & How to use ?

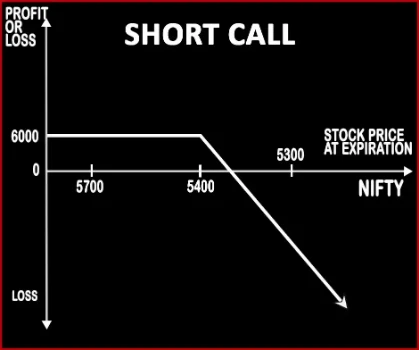

SHORT CALL

RATIO PUT WRITE

Market View

Bearish

Neutral

When to use?

It is an aggressive strategy and involves huge risks. It should be used only in case where trader is certain about the bearish market view on the underlying.

This strategy is implemented by selling (short) the underlying asset in the cash/futures market. This strategy is used by a trader who in neutral on the market and bearish on the volatility in the near future

Action

Sell or Write Call Option

Sell 2 ATM Puts

Breakeven Point

Strike Price of Short Call + Premium Received

Upper Breakeven Point = Strike Price of Short Puts + Points of Maximum Profit Lower Breakeven Point = Strike Price of Short Puts - Points of Maximum Profit

SHORT CALL Vs RATIO PUT WRITE - Risk & Reward

SHORT CALL

RATIO PUT WRITE

Maximum Profit Scenario

Max Profit = Premium Received

Net Premium Received - Commissions Paid

Maximum Loss Scenario

Loss Occurs When Price of Underlying > Strike Price of Short Call + Premium Received

Price of Underlying - Sale Price of Underlying - Net Premium Received OR Strike Price of Short Put - Price of Underlying - Net Premium Received + Commissions Paid

Risk

Unlimited

Unlimited

Reward

Limited

Limited

SHORT CALL Vs RATIO PUT WRITE - Strategy Pros & Cons

SHORT CALL

RATIO PUT WRITE

Similar Strategies

Covered Put, Covered Calls

Short Strangle and Short Straddle

Disadvantage

• Unlimited risk to the upside underlying stocks. • Potential loss more than the premium collected.

• Potential loss is higher than gain. • Limited profit.

Advantages

• With the help of this strategy, traders can book profit from falling prices in the underlying asset. • Less investment, more profit. • Traders can book profit when underlying stock price fall, move sideways or rise by a small amount.