Compare Strategies

| SHORT STRANGLE | BULL CALENDER SPREAD | |

|---|---|---|

|

|

|

| About Strategy |

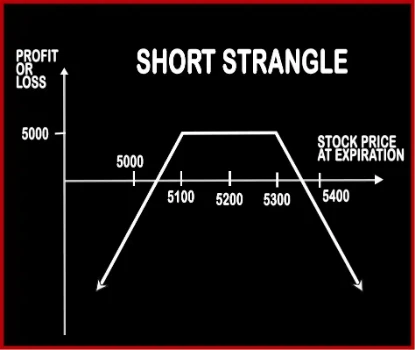

Short Strangle Option StrategyThis strategy is similar to Short Straddle; the only difference is of the strike prices at which the positions are built. Short Strangle involves selling of one OTM Call Option and selling of one OTM Put Option, of the same expiry date and same underlying asset. Here the probability of making profits is more as there is a spread between the two strike prices, and if |

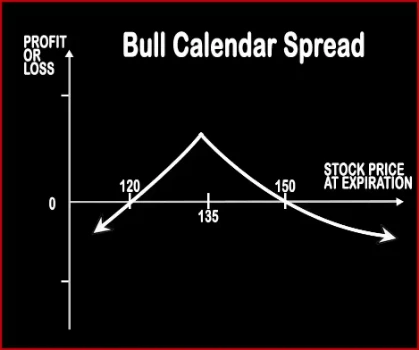

Bull Calendar Spread Option StrategyThis strategy is implemented when a trader is bullish on the underlying stock/index in the short term say 2 months or so. A trader will write one Near Month OTM Call Option and buy one next Month OTM Call Option, thereby reducing the cost of purchase, with the same strike price of the same underlying asset. This strategy is used when a trader wants to make prof .. |

SHORT STRANGLE Vs BULL CALENDER SPREAD - Details

| SHORT STRANGLE | BULL CALENDER SPREAD | |

|---|---|---|

| Market View | Neutral | Bullish |

| Type (CE/PE) | CE (Call Option) + PE (Put Option) | CE (Call Option) + PE (Put Option) |

| Number Of Positions | 2 | 2 |

| Strategy Level | Advance | Beginners |

| Reward Profile | Limited | Unlimited |

| Risk Profile | Unlimited | Limited |

| Breakeven Point | Lower Break-even = Strike Price of Put - Net Premium, Upper Break-even = Strike Price of Call+ Net Premium | Stock Price when long call value is equal to net debit. |

SHORT STRANGLE Vs BULL CALENDER SPREAD - When & How to use ?

| SHORT STRANGLE | BULL CALENDER SPREAD | |

|---|---|---|

| Market View | Neutral | Bullish |

| When to use? | This strategy is perfect in a neutral market scenario when the underlying is expected to be less volatile. | This strategy is used when a trader wants to make profit from a steady increase in the stock price over a short period of time. |

| Action | Sell OTM Call, Sell OTM Put | Sell 1 Near-Term OTM Call, Buy 1 Long-Term OTM Call |

| Breakeven Point | Lower Break-even = Strike Price of Put - Net Premium, Upper Break-even = Strike Price of Call+ Net Premium | Stock Price when long call value is equal to net debit. |

SHORT STRANGLE Vs BULL CALENDER SPREAD - Risk & Reward

| SHORT STRANGLE | BULL CALENDER SPREAD | |

|---|---|---|

| Maximum Profit Scenario | Maximum Profit = Net Premium Received | You have unlimited profit potential to the upside. |

| Maximum Loss Scenario | Loss = Price of Underlying - Strike Price of Short Call - Net Premium Received | Max Loss = Premium Paid + Commissions Paid |

| Risk | Unlimited | Limited |

| Reward | Limited | Unlimited |

SHORT STRANGLE Vs BULL CALENDER SPREAD - Strategy Pros & Cons

| SHORT STRANGLE | BULL CALENDER SPREAD | |

|---|---|---|

| Similar Strategies | Short Straddle, Long Strangle | The Collar, Bull Put Spread |

| Disadvantage | • Unlimited loss is associated with this strategy, not recommended for beginners. • Limited reward amount. | • Limited profit even if underlying asset rallies. • If the short call options are assigned when the underlying asset rallies then losses can be sustained. |

| Advantages | • Higher chance of profitability due to selling of OTM options. • Advantage from double time decay and a contraction in volatility. • Traders can book profit when underlying asset stays within a tight trading range. | • Limited losses to the net debit. • Enable trader to book profit even if underlying asset stays stagnant. • If the market trends reverse, cashing in from stock price movement at limited risk. |