Compare Strategies

| SHORT STRANGLE | COVERED CALL | |

|---|---|---|

|

|

|

| About Strategy |

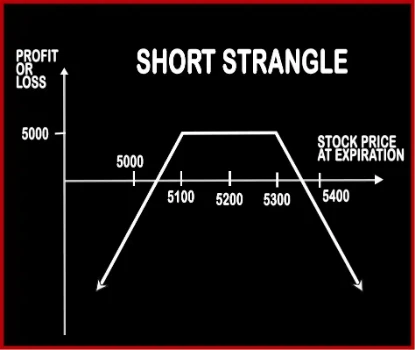

Short Strangle Option StrategyThis strategy is similar to Short Straddle; the only difference is of the strike prices at which the positions are built. Short Strangle involves selling of one OTM Call Option and selling of one OTM Put Option, of the same expiry date and same underlying asset. Here the probability of making profits is more as there is a spread between the two strike prices, and if |

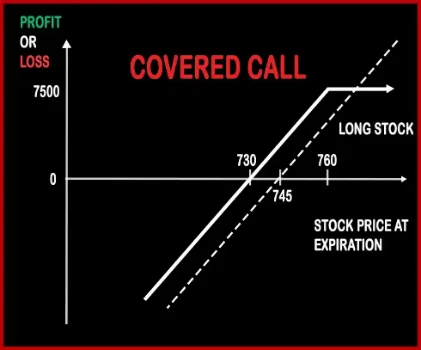

Covered Call Option StrategyMr. X owns Reliance Shares and expects the price to rise in the near future. Mr. X is entitled to receive dividends for the shares he hold in cash market. Covered Call Strategy involves selling of OTM Call Option of the same underlying asset. The OTM Call Option Strike Price will generally be the price, where Mr. X will look to get out o .. |

SHORT STRANGLE Vs COVERED CALL - Details

| SHORT STRANGLE | COVERED CALL | |

|---|---|---|

| Market View | Neutral | Bullish |

| Type (CE/PE) | CE (Call Option) + PE (Put Option) | CE (Call Option) |

| Number Of Positions | 2 | 2 |

| Strategy Level | Advance | Advance |

| Reward Profile | Limited | Limited |

| Risk Profile | Unlimited | Unlimited |

| Breakeven Point | Lower Break-even = Strike Price of Put - Net Premium, Upper Break-even = Strike Price of Call+ Net Premium | Purchase Price of Underlying- Premium Received |

SHORT STRANGLE Vs COVERED CALL - When & How to use ?

| SHORT STRANGLE | COVERED CALL | |

|---|---|---|

| Market View | Neutral | Bullish |

| When to use? | This strategy is perfect in a neutral market scenario when the underlying is expected to be less volatile. | An investor has a short term neutral view on the asset and for this reason holds the asset long and has a short position to generate income. |

| Action | Sell OTM Call, Sell OTM Put | (Buy Underlying) (Sell OTM Call Option) |

| Breakeven Point | Lower Break-even = Strike Price of Put - Net Premium, Upper Break-even = Strike Price of Call+ Net Premium | Purchase Price of Underlying- Premium Received |

SHORT STRANGLE Vs COVERED CALL - Risk & Reward

| SHORT STRANGLE | COVERED CALL | |

|---|---|---|

| Maximum Profit Scenario | Maximum Profit = Net Premium Received | [Call Strike Price - Stock Price Paid] + Premium Received |

| Maximum Loss Scenario | Loss = Price of Underlying - Strike Price of Short Call - Net Premium Received | Purchase Price of Underlying - Price of Underlying) + Premium Received |

| Risk | Unlimited | Unlimited |

| Reward | Limited | Limited |

SHORT STRANGLE Vs COVERED CALL - Strategy Pros & Cons

| SHORT STRANGLE | COVERED CALL | |

|---|---|---|

| Similar Strategies | Short Straddle, Long Strangle | Bull Call Spread |

| Disadvantage | • Unlimited loss is associated with this strategy, not recommended for beginners. • Limited reward amount. | • Unlimited risk, limited reward. • Inability to earn interest on the proceed used to buy the underlying stock. |

| Advantages | • Higher chance of profitability due to selling of OTM options. • Advantage from double time decay and a contraction in volatility. • Traders can book profit when underlying asset stays within a tight trading range. | • Profit from option premium, rise in the underlying stock and dividends on the stock. • Allows you to generate income from your holding. • Profit when underlying stock price rise, move sideways or marginal fall. |