Compare Strategies

| RATIO CALL SPREAD | SYNTHETIC LONG CALL | |

|---|---|---|

|

|

|

| About Strategy |

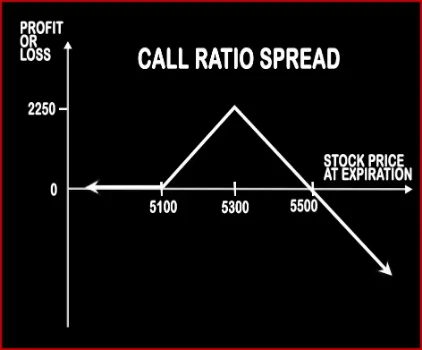

Ratio Call Spread Option StrategyAs the name suggests, a ratio of 2:1 is followed i.e. buy 1 ITM Call and simultaneously sell OTM Calls double the number of ITM Calls (In this case 2). This strategy is used by trader who is neutral on the market and bearish on the volatility in the near future. Here profits will be capped up to the premium amount and risk will be potentially unlimited since he is |

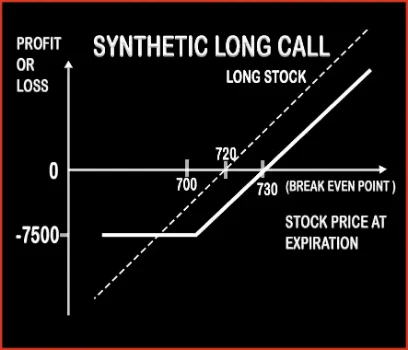

Synthetic Long Call Option StrategyA trader is bullish in nature for short term, but also fearful about the downside risk associated with it. Here, a trader wants to hold an underlying asset either in physical form like in case of commodities or demat (electronic) form in case of stocks. But he is always exposed to downside risk and in order to mitigate his losses, .. |

RATIO CALL SPREAD Vs SYNTHETIC LONG CALL - Details

| RATIO CALL SPREAD | SYNTHETIC LONG CALL | |

|---|---|---|

| Market View | Neutral | Bullish |

| Type (CE/PE) | CE (Call Option) | CE (Call Option) |

| Number Of Positions | 3 | 2 |

| Strategy Level | Beginners | Beginners |

| Reward Profile | Limited | When Price of Underlying > Purchase Price of Underlying + Premium Paid |

| Risk Profile | Unlimited | Limited (Maximum loss happens when the price of instrument move above from the strike price of put) |

| Breakeven Point | Upper Breakeven Point = Strike Price of Short Calls + (Points of Maximum Profit / Number of Uncovered Calls), Lower Breakeven Point = Strike Price of Long Call +/- Net Premium Paid or Received | Underlying Price + Put Premium |

RATIO CALL SPREAD Vs SYNTHETIC LONG CALL - When & How to use ?

| RATIO CALL SPREAD | SYNTHETIC LONG CALL | |

|---|---|---|

| Market View | Neutral | Bullish |

| When to use? | This strategy is used by trader who is neutral on the market and bearish on the volatility in the near future. Here profits will be capped up to the premium amount and risk will be potentially unlimited since he is selling two calls. | A trader is bullish in nature for short term, but also fearful about the downside risk associated with it. |

| Action | Buy 1 ITM Call, Sell 2 OTM Calls | Buy 1 ATM Put or OTM Put |

| Breakeven Point | Upper Breakeven Point = Strike Price of Short Calls + (Points of Maximum Profit / Number of Uncovered Calls), Lower Breakeven Point = Strike Price of Long Call +/- Net Premium Paid or Received | Underlying Price + Put Premium |

RATIO CALL SPREAD Vs SYNTHETIC LONG CALL - Risk & Reward

| RATIO CALL SPREAD | SYNTHETIC LONG CALL | |

|---|---|---|

| Maximum Profit Scenario | Strike Price of Short Call - Strike Price of Long Call + Net Premium Received - Commissions Paid | Current Price - Purchase Price - Premium Paid |

| Maximum Loss Scenario | Price of Underlying - Strike Price of Short Calls - Max Profit + Commissions Paid | Premium Paid |

| Risk | Unlimited | Limited |

| Reward | Limited | Unlimited |

RATIO CALL SPREAD Vs SYNTHETIC LONG CALL - Strategy Pros & Cons

| RATIO CALL SPREAD | SYNTHETIC LONG CALL | |

|---|---|---|

| Similar Strategies | Variable Ratio Write | Protective Put, Long Call |

| Disadvantage | • Unlimited potential loss. • Complex strategy with limited profit. | •Chances of loss if the underlying goes down. •Incur losses if option is exercised. |

| Advantages | • Downside risk is almost zero. • Investors can book profit from share prices moving within given limits. • Trader can maximise profit when the share closes at the upper breakeven point. | •Limited risk, unlimited profit. •Protection to your long-term holdings. • Limited loss to the to the premium paid for Put option. |